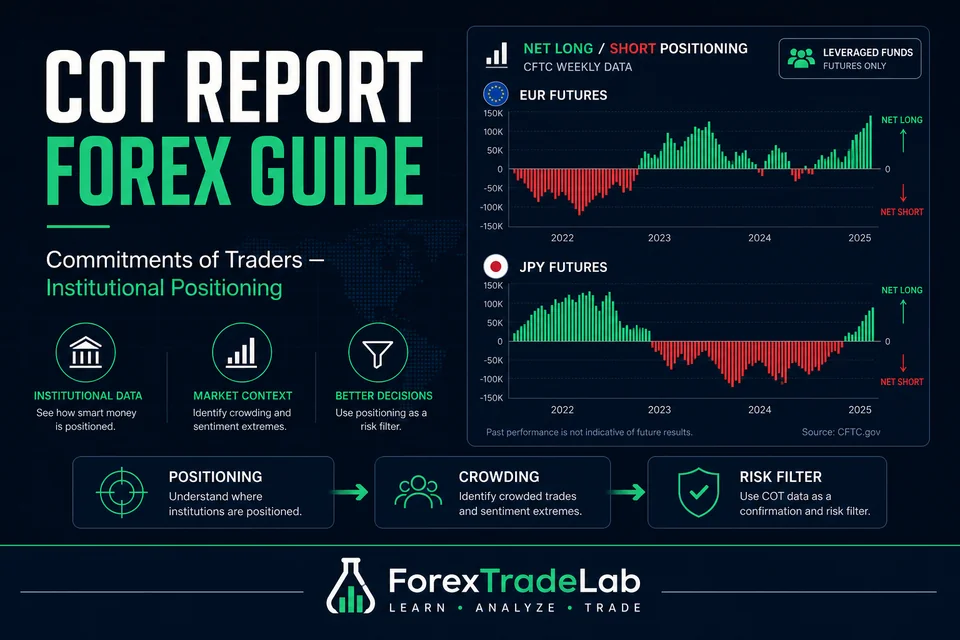

- The COT report shows net long/short positioning of reportable futures traders — it is a positioning snapshot, not a price forecast

- For forex, track CME currency futures (EUR, GBP, JPY, CAD, AUD, CHF, MXN) and COMEX gold — not every spot pair has a direct futures line

- Extreme speculative positioning often marks late-stage trends or crowded trades vulnerable to sharp reversals

- Commercial hedgers and leveraged funds read differently — commercials hedge business risk; specs express directional bets

- The highest-value use of COT is filtering: avoid adding size when your thesis aligns with an already-crowded speculative extreme

Trusted by 20M+ traders — open your account in minutes

- Trade 1,400+ instruments

- Country-based bonus offers where eligible

- MT4 & MT5 available

- Easy deposits and withdrawals

- Leverage up to 1000:1, where available

- Copy Trading: auto-copy expert strategy managers

June 2026 field note: Positioning data lags by several days and describes futures, not the entire $7.5 trillion OTC spot market. Use COT as context for risk sizing — not as a standalone entry signal.

TL;DR — COT for Forex Traders#

| Question | Answer |

|---|---|

| What does COT measure? | Net long/short futures positions by participant category |

| When released? | Weekly (Friday), data as of prior Tuesday |

| Best contracts for FX? | CME currency futures + COMEX gold |

| Who to watch? | Leveraged funds / non-commercial speculators |

| Main use case? | Spot crowded trades and squeeze risk |

| Main mistake? | Treating extreme readings as automatic reversals |

If you trade forex with real capital — especially swing or position horizons — you are not trading in a vacuum. Somewhere between your retail platform and the interbank market, banks, hedge funds, and corporate hedgers are building and unwinding exposure. The COT report is one of the few public, weekly windows into that positioning on regulated futures.

This guide explains how to read it without the mystique.

What the COT Report Actually Is#

The US Commodity Futures Trading Commission (CFTC) requires large traders in regulated US futures markets to report positions above reporting thresholds. Each week, the CFTC aggregates those reports and publishes the Commitments of Traders (COT) data.

Important distinctions retail traders miss:

- It is futures positioning, not spot FX volume. The global spot forex market trades mostly OTC. CME currency futures are a liquid but smaller slice — yet institutional participants use them, so positioning still carries information.

- It is a snapshot with lag. Positions are as of Tuesday close; you receive them on Friday. Price can move significantly before you see the report.

- Categories mean different things. A commercial exporter hedging EUR revenue is not "betting against the euro" the way a hedge fund shorting EUR futures is.

The CFTC's own explanatory page stresses that the report describes market composition, not a trading recommendation.

Which Contracts Matter for Forex Traders#

| CME / COMEX contract | Spot FX relevance | Typical use |

|---|---|---|

| Euro FX (EUR/USD) | EUR/USD | Euro trend & ECB/Fed positioning |

| British Pound (GBP/USD) | GBP/USD | Sterling risk, BoE cycle |

| Japanese Yen (JPY/USD) | USD/JPY (inverse) | Carry trade & BoJ policy |

| Australian Dollar | AUD/USD | Commodity FX, risk-on proxy |

| Canadian Dollar | USD/CAD | Oil-linked CAD flows |

| Swiss Franc | USD/CHF | Safe-haven CHF positioning |

| Mexican Peso | USD/MXN | EM carry & US-Mexico macro |

| Gold (COMEX) | XAU/USD | Safe haven vs real yields |

For session and liquidity context when you act on macro positioning, pair this with our forex market hours and slippage guide.

How to Read the Three Main Categories#

Commercial traders#

Who: Banks, exporters, importers, producers hedging real-world currency exposure.

How to read: Extreme commercial positioning often reflects hedging demand, not a forecast. If US importers are heavily long EUR futures, they may be hedging euro-denominated costs — not calling a euro rally.

Non-commercial / leveraged funds#

Who: Hedge funds, CTAs, large speculators.

How to read: This is the category most forex traders monitor. Rising net long EUR positioning means speculators as a group are adding bullish EUR exposure. Extreme net long or net short vs. a 3–5 year range is the key signal — not the absolute number.

Non-reportable / small traders#

Who: Positions below reporting thresholds.

How to read: Often used as a contrarian input (retail leaning the wrong way at extremes). Treat with caution — the category is noisy and smaller than fund positioning.

The Setup: Net Positioning vs. Price#

The standard workflow serious traders use:

- Plot net non-commercial positioning (or leveraged funds in disaggregated data) as a line chart.

- Overlay price of the corresponding currency pair.

- Mark percentile bands — e.g. is current positioning above the 90th percentile of the last 156 weeks (3 years)?

Worked example — reading crowding (illustrative)#

Suppose leveraged funds hold a net long EUR position near the top of a 3-year range while EUR/USD has already rallied 8% over six months and the ECB has shifted to a cautious hold while markets price Fed cuts.

| COT reading | Price context | Risk interpretation |

|---|---|---|

| Net long at 90th percentile | Trend mature, little fresh catalyst | New longs are crowded; squeeze risk on hawkish Fed surprise |

| Net long rising, mid-range | Trend early, rate differential widening | Positioning supports trend; crowding not yet extreme |

| Net long falling from extreme | Price consolidating | Unwind in progress; trend may be exhausting |

This is filter logic, not entry logic. Entry still comes from your strategy — structure, levels, event calendar.

COT and the Yen: Why Carry Traders Should Care#

No currency illustrates COT's value better than the yen. The carry trade borrows low-yield JPY to fund higher-yield assets. That flow shows up as speculative short JPY positioning in futures.

When positioning becomes historically stretched short JPY:

- The carry trade earns daily swap income — until it doesn't.

- Any BoJ surprise or global risk-off event can force simultaneous covering of yen shorts.

- The move is violent because positioning is one-directional.

The July–August 2024 yen surge after BoJ policy signals was preceded by extreme short-yen positioning in COT data — not as a perfect timer, but as a risk flag that the trade was crowded. Traders who treated carry income as "free money" without monitoring positioning learned an expensive lesson.

For the rates channel behind yen moves, see how interest rates affect forex.

Combining COT With Your Existing Toolkit#

COT works best as a layer, not a strategy:

| Your tool | What COT adds |

|---|---|

| Technical structure (SMC, support/resistance) | Know if you are trading with or against institutional crowding |

| Interest-rate differential / carry | Flag when carry is crowded in positioning data |

| Economic calendar | Avoid adding before events when positioning is already extreme |

| Correlation / portfolio risk | See if multiple "different" trades are one positioning bet |

If you run multiple USD-short positions (long EUR/USD, long GBP/USD, long AUD/USD), COT on each contract plus our correlation guide prevents hidden concentration.

Five Mistakes That Waste COT Data#

- Fading every extreme immediately. Extremes can become more extreme in strong macro trends.

- Ignoring the release lag. Tuesday's positioning may already be stale by Friday.

- Using spot-only pairs with no futures line. There is no direct COT for many exotics — do not invent data.

- Confusing commercials with speculators. Hedging flow is not a directional bet.

- Replacing risk management with COT. A crowded trade can still move 500 pips against you before reversing.

A Simple Weekly COT Routine (30 Minutes)#

Friday after COT release:

- Check net leveraged-fund positioning on your 2–3 core pairs.

- Note any reading above 85th or below 15th percentile (3-year lookback).

- Cross-check the next week's central-bank calendar.

- Adjust risk budget — not necessarily direction:

- Crowded + aligned with your bias → reduce size or widen invalidation awareness.

- Crowded + against your bias → be patient; reversals need a catalyst.

- Neutral positioning → let your primary strategy lead.

Log the reading in your trading journal. Over 6–12 months you will see how positioning extremes correlated with your own P&L — that personalised dataset beats any generic COT rule.

Risk reminder: This article is educational only — not investment advice or a trade recommendation. Futures positioning can diverge from spot flows, and past positioning extremes do not guarantee future reversals. Always size positions so that a single macro surprise cannot compromise your account.

Comments

Add a useful note for other traders. We review comments before publishing.